8 minutes 01 Mar 2024

This is the second post in the series “The Promise of Blockchain.” If you haven’t read the others, you can find them here.

2008, the year the global economy went skydiving without a parachute. Banks were handing out mortgages like they were free samples at a shopping center.

Back then, borrowers could get 100% mortgages without proving any income, jobs, or assets. NINJA loans (no income, no job, and no assets) is what they were called, and they significantly contributed to the subprime mortgage crisis. Risky mortgages like these were bundled into complex financial instruments and sold to investors worldwide. When the housing market eventually crashed, these securities tanked in value, leading to huge financial losses.

People lost their jobs, their homes, and watched their life savings evaporate.

This crisis exposed significant flaws in the financial system, particularly the lack of transparency, which hid the risks associated with these complex financial instruments. The centralization of power within a handful of large financial institutions concentrated risk, meaning that the failure of one institution could trigger a systemic crisis. And as we know, that’s exactly what happened.

These were grim times and needed government intervention to bail out the banks deemed “too big to fail.” While this intervention brought some stability, it also led to serious public distrust in traditional financial institutions. It was during this period of uncertainty and distrust that Satoshi Nakamoto published the Bitcoin white paper on October 31, 2008.

The Birth of Bitcoin

Nobody knows the real identity of Satoshi Nakamoto. We don’t even know if this name refers to an individual or a group of people. All we know is that the timing of Bitcoin’s introduction was almost perfect: it came out during a crisis of trust in financial institutions, almost like a middle finger to centralized power in the financial system. Bitcoin offered an innovative alternative when the world was primed for new financial solutions.

You’ve probably seen, or even know, people who’ve made massive gains from buying Bitcoin. But Bitcoin wasn’t made for speculation or investment purposes. In simple terms, Bitcoin was designed to enable direct payments between parties without the need for a central authority like a bank or financial institution. But what is Bitcoin?

Blockchain or Cryptocurrency

Bitcoin is both a blockchain network and the name of the digital currency that operates on that network. You can think of Bitcoin as a huge, global system - like the internet, but specifically for a digital currency. This system includes all the computers running Bitcoin software, the rules they follow, and the connections between them. This is the Bitcoin network.

The digital “coins” that people buy, sell, and trade are also called Bitcoin. These Bitcoin exist as entries in a distributed ledger on the Bitcoin network. When we say Bitcoins are “sent” or “received,” what’s actually happening is that the ledger is being updated to reflect changes in account balances. There are no physical coins or even individual digital tokens moving around - it’s all about adjusting numbers in this shared, decentralized ledger.

So if we say “Bitcoin operates on a network,” we’re actually talking about Bitcoin (the crypto currency) operating on the Bitcoin network. It’s a bit like saying “email operates on the internet” - email is both the system(technically called SMTP) and the thing being sent through that system.

This dual nature of Bitcoin being both a network and a currency isn’t unique to Bitcoin. It’s a common thing in the blockchain world. Some blockchain networks have what’s called a native token, like Bitcoin, which is usually named after the network itself. The native token acts as a reward for the computers (nodes) that keep the network running, is used to pay transaction fees on the network, and it often functions as a tradable digital asset. Think of it as the ‘official currency’ of that particular blockchain network.

In some other cases the native token will have a name that is different to the name of the network. For example, Ethereum, another blockchain network we’ll talk about in future posts, has a native token called Ether serving similar functions there as Bitcoin does on its network.

As a decentralized digital currency, Bitcoin’s potential to facilitate financial transactions becomes clear when we look at real-world scenarios.

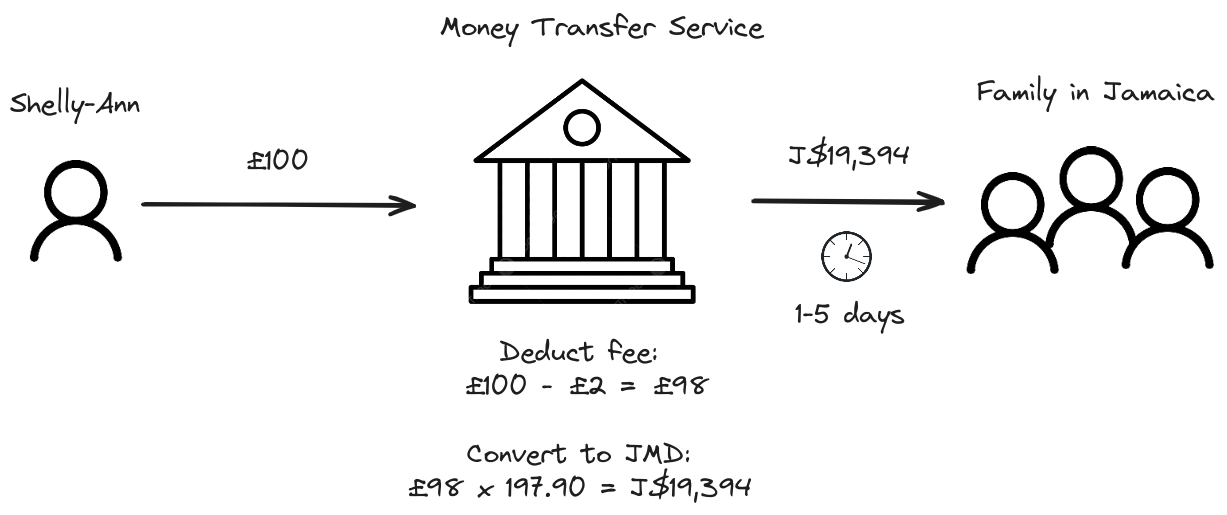

Shelly-Ann’s Story

Shelly-Ann, a 32-year-old second generation Jamaican immigrant living in London, sends £100 monthly to her family in Jamaica via a high street money transfer service. Here’s how it breaks down:

- The money transfer service deducts a transfer fee of £2

- They use their exchange rate: 1 GBP = 197.90 JMD (vs. mid-market rate of 1 GBP = 200.911 JMD) to convert the pounds to Jamaican dollars

- Amount received: 19,394 JMD

The transfer would usually be completed in about 1-5 days.

Shelly-Ann loses about £3.47 to fees and exchange rate markup. £98 worth of Jamaican dollars (at the transfer service’s exchange rate) reaches her family, which is equivalent to £96.53 at the true exchange rate, despite her sending £100. These numbers were taken from the transfer calculator on the JN money transfer website. Whether or not this transfer is expensive is subjective, but you could think about how much it would cost you to transfer the same amount in your home country to a friend.

The key points here are:

- There is a reliance on a centralised service. Money transfer services, or any middleman, can charge whatever fees they want to facilitate the transfer. These fees are usually higher for remote or less developed countries.

- The transfer time is long. This could be problematic especially in times of emergency

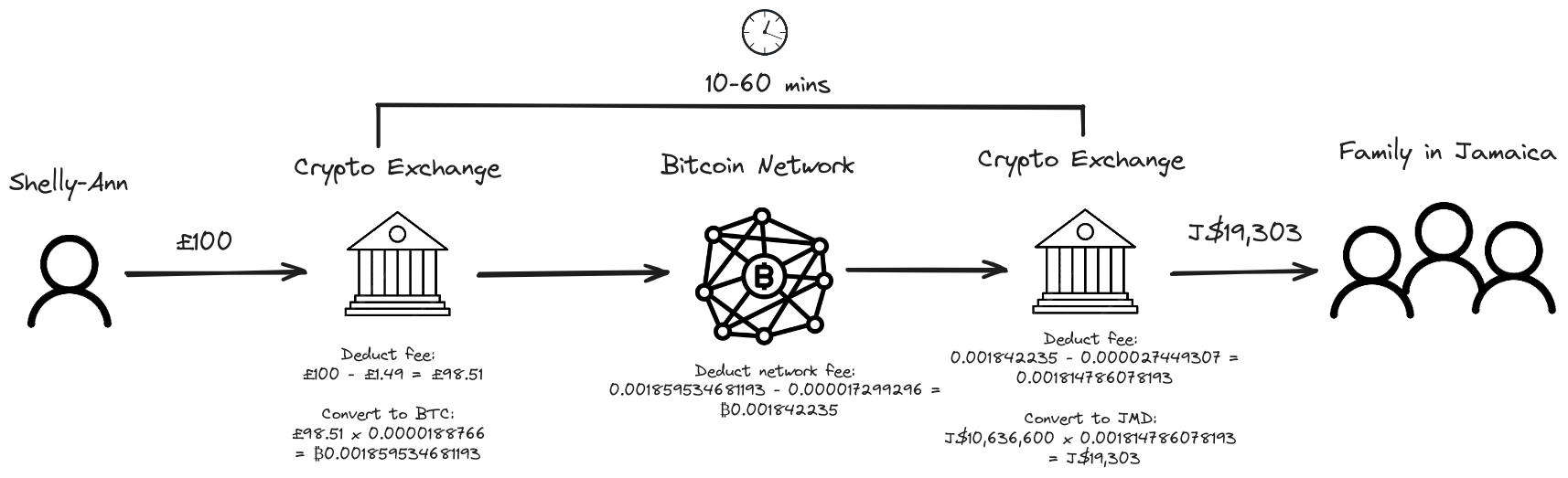

If Shelly-Ann were to use Bitcoin instead, she would need to do the following:

-

Buy Bitcoin using a crypto exchange: These platforms, similar to high street currency exchanges, operate online and allow people to exchange fiat currencies for cryptocurrencies and vice-versa. Examples include Kraken, Coinbase, and Binance. The fees for buying Bitcoin vary depending on the platform and payment method used. For example, using a bank transfer might incur fees around 0.1% to 1.49%, while using a credit or debit card could result in higher fees, sometimes between 3.5% and 5%.

-

Send Bitcoin to her family’s Bitcoin wallet in Jamaica: This transaction would include a network fee which, at the time of writing, is on average $1.12 (about 0.000017299296 BTC)

-

Sell Bitcoin for Jamaican Dollars: Once the family receives the Bitcoin, they would need to sell it for Jamaican dollars using a local crypto exchange, which would charge similar fees to buying Bitcoin

Here’s how her £100 transfer might look:

- Exchange fee to buy Bitcoin with GBP: £1.49 (1.49% fee)

- GBP to BTC exchange rate: 1 GBP = 0.0000188766 BTC

- BTC Received: 0.001859534681193 BTC

- Bitcoin network fee: 0.000017299296 BTC

- Exchange fee to sell Bitcoin for JMD: 0.000027449307 BTC (1.49% of remaining BTC)

- BTC amount after fees: 0.001814786078193 BTC

- BTC to JMD exchange rate: 1 BTC = 10,636,600 JMD

- Final JMD received: 19,303 JMD

The transfer would usually be completed in about 10-60 minutes.

The time a Bitcoin transfer takes depends on a couple of factors. This article does a good job of explaining them.

In this example, the fees lost were still minimal (just under £5), but we are still in the same situation as before. The transfer still relies on centralized services at both ends of the transaction who can set whatever fees they want and in some cases deny service to users based on where they live or other factors. The Bitcoin network fee is also variable and instead of being set by a centralized entity, depends on the network usage. So in times of high traffic the network fee could be much higher.

Additionally, the volatility of Bitcoin can significantly impact the value of the transferred amount, with potential losses if the price drops during the transaction period. To address these issues, stablecoins were introduced. Stablecoins are cryptocurrencies pegged to stable assets like the US dollar, which help get around the volatility risk associated with Bitcoin(and other crypto currencies), ensuring a more predictable value during transactions. Stablecoins are a great appliation of blockchain technology which we will explore in a future post.

Comparison

Here’s a comparison of the traditional money transfer vs. Bitcoin transfers:

| Aspect | Traditional Money Transfer | Bitcoin Transfer |

|---|---|---|

| Speed | 1-5 days | 10-60 minutes |

| Complexity | Simple, familiar process | More complex, requires technical knowledge |

| Cost (in this example) | £3.47 in fees and exchange rate markup | About £4.97 in total fees |

| Reliance on centralized services | Single centralized service | Multiple centralized exchanges |

| Volatility | Stable | Subject to market fluctuations |

| Adoption | Widely accepted | Limited adoption |

| Regulatory clarity | Well-established regulations | Evolving regulatory landscape |

This comparison shows that while Bitcoin offers some advantages like speed, it also comes with its own set of challenges. The current state of crypto adoption means that fully realizing Satoshi Nakamoto’s vision of peer-to-peer electronic cash without intermediaries is still a work in progress.

Future Improvements and Alternatives

While Bitcoin faces challenges for everyday transactions, the blockchain space continues to evolve. Developments like the Lightning Network aim to make Bitcoin transactions faster and cheaper. Other blockchains, such as Ripple and Stellar focus on international transfers, while stablecoins like Mento cUSD and Tether USDT address volatility concerns. These look promising, but also face their own hurdles in realizing Satoshi’s vision of efficient, decentralized value transfer.

Conclusion

Shelly-Ann’s story shows the potential benefits and current limitations of using Bitcoin for international transfers, it’s just one example of how this technology can be applied. To really appreciate the nature of Bitcoin, we need to look a bit deeper into its technical foundations.

Bitcoin’s emergence following the 2008 financial crisis wasn’t coincidental, it was a response to a flawed system. From its mysterious origins to potential real-world applications like Shelly-Ann’s case, Bitcoin represents a paradigm shift in financial transactions and trust. While facing adoption challenges and technical hurdles, its core features—blockchain foundation, peer-to-peer network, and limited supply—address many issues exposed by the crisis, offering an alternative to traditional finance’s opacity and centralized control. As the technology evolves, new solutions are emerging to address additional challenges like scalability, further expanding blockchain’s potential. In the next post, we’ll look at Bitcoin’s fundamental features, exploring how they work and why they matter in reshaping our financial future.

If you want to stay updated with the latest posts, consider subscribing to my newsletter. You can do this by clicking the button below.

Liked this post? Share it using the links below